This ZATCA guideline clarifies the Value Added Tax (VAT) treatment for transactions involving agents in the Kingdom of Saudi Arabia. It provides a detailed framework for distinguishing between an agent acting as a principal versus one acting on behalf of a principal. The guide primarily explains the application of Article 9 of the KSA VAT Law, which deems an agent acting in their own name (undisclosed) as the supplier or receiver of goods or services for VAT purposes. It further covers tax invoicing, input VAT deduction, disbursements, reimbursements, and special cases for sectors like travel and finance.

Agents

VAT Guideline | Version One

July 2020

Contents

1. Introduction

1.1. Implementing a Value Added Tax (VAT) system in the Kingdom of Saudi Arabia (KSA)

1.2. Zakat, Tax and Customs Authority (ZATCA)

1.3. What is Value Added Tax?

1.4. This Guideline

2. Definitions of the main terms used

3. Economic Activity and Registration

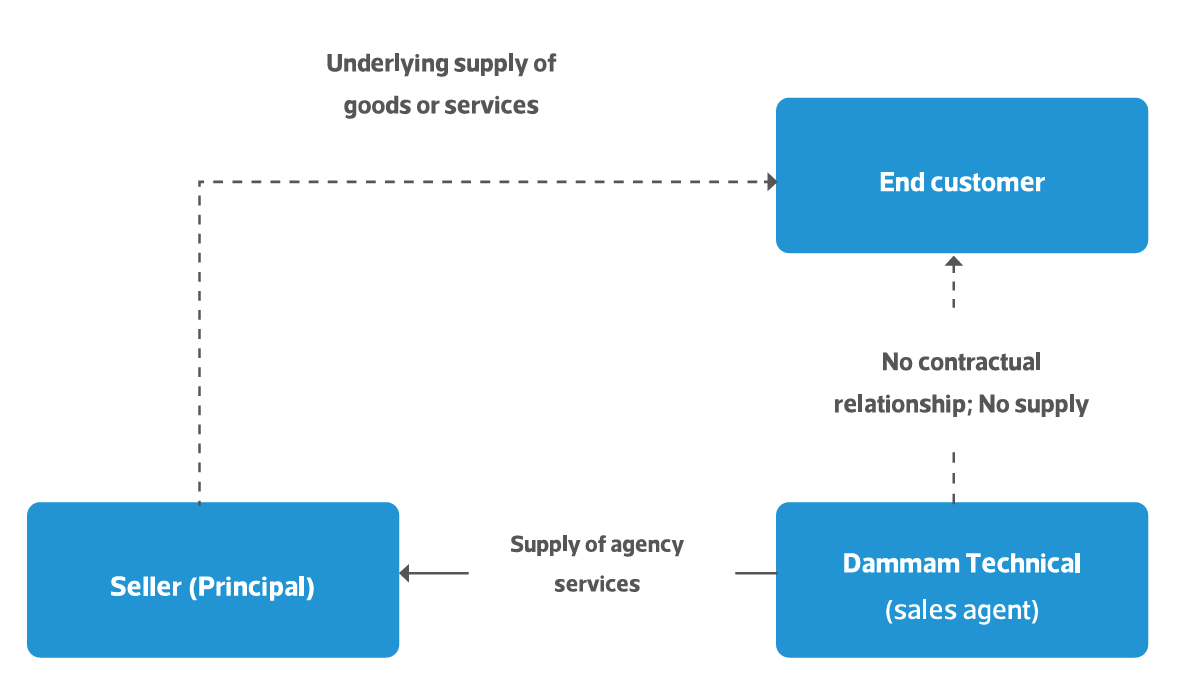

It will receive a commission or other remuneration for carrying out these services. This is a supply of services, which is separate to the underlying supply it arranges on behalf of the Principal. For this supply, the Agent acts as a Supplier, and the Principal as a Customer.

Continue Reading

Access Full Content

You're viewing a preview of this document. Please log in to unlock the complete content, annotations, and research tools.

Click here to view details of the free plan and the subscriptions we offer.