Beta Version

Website Last updated:

July 17, 2026

Simplified Guide

The Decision to Reclassify the Value-Added Tax Field Violations

Zakat, Tax and Customs Authority

January 30, 2022

Contents

1. Highlights of the Decision

2. What Is Not Covered by the Decision?

3. Classification of Violations According to the New Decision

4. Illustrative Examples of the Decision to Reclassify VAT Violations

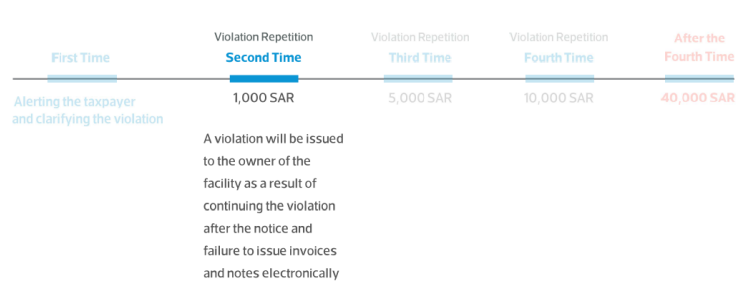

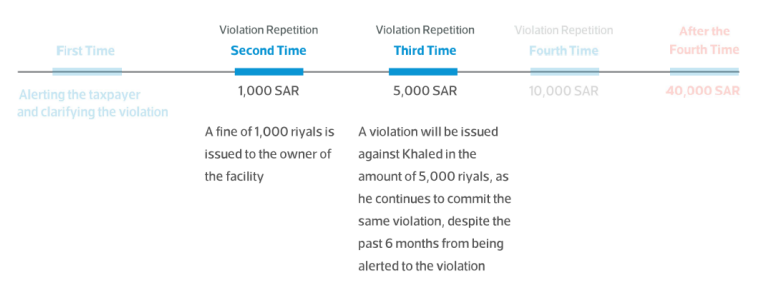

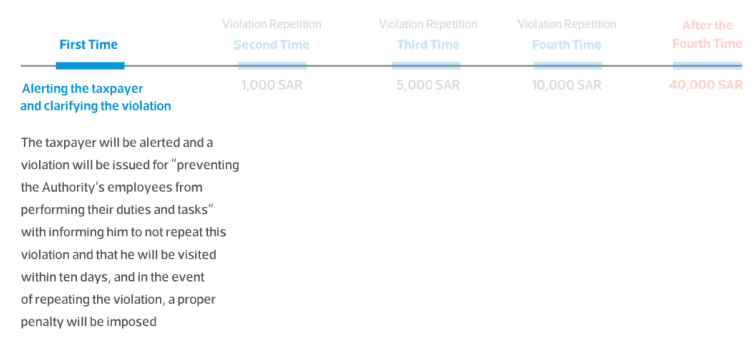

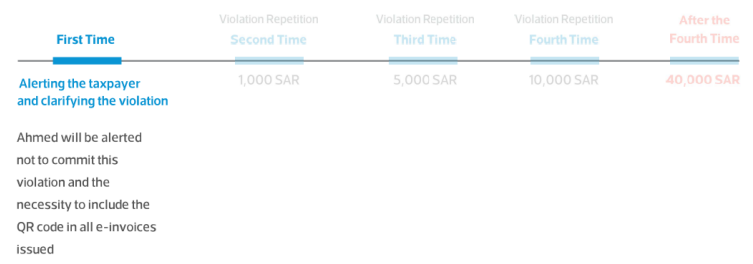

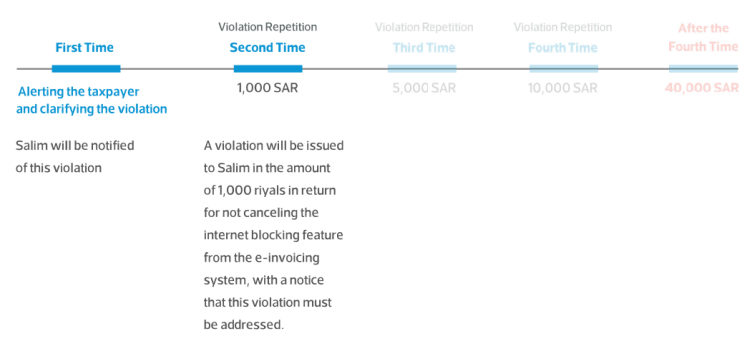

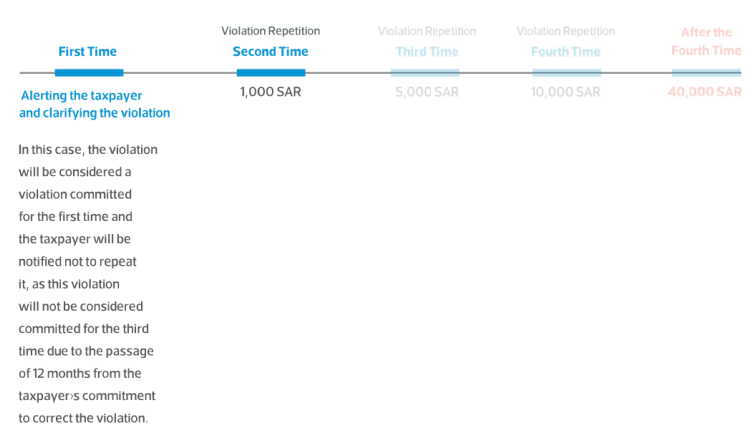

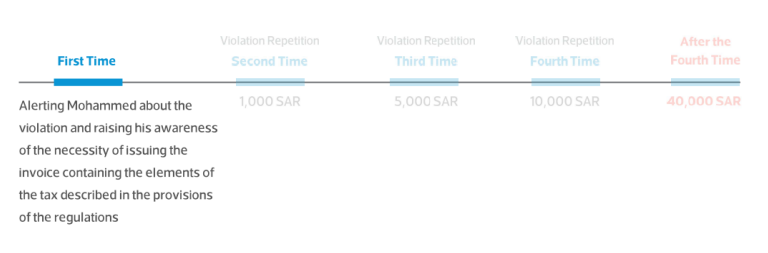

First: Violation of non-compliance to issue a tax invoice